Saving, investing, and planning for retirement can be an exercise in futility if an individual lacks the know-how that is required to be successful, according to the seventh annual Aegon Retirement Readiness Survey.

While many people may not have the desire or wherewithal to become retirement experts themselves, they must be able to recognise and rely on sound advice.

According to the report:

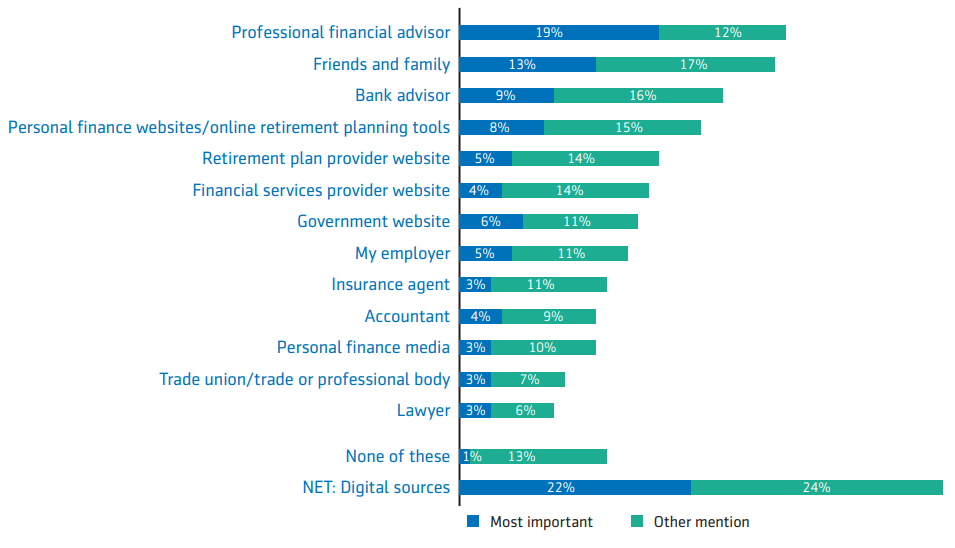

Globally, people are using or say they would use a variety of sources of information and advice when choosing how to save for retirement.

Sources of information and advice for retirement savings

Source: Aegon Retirement Readiness Survey 2018

The most frequently cited source is professional financial advisers (32%), closely followed by family and friends (30%). Among possible sources, professional financial advisers are most likely to be deemed most important (19%).

The internet has become a major source for information with 46% using or indicating that they would use some form of digital source of information and advice. The penetration is greatest in emerging markets, such as India, China and Turkey, where alternative sources may not be as commonplace or accessible. It is lowest in France and Spain where people are generally less engaged with retirement planning.

The ability to successfully navigate through the vast amounts of information available online and recognise the difference between reliable and unreliable sources requires that people be financially literate.

Read:

MDRT 2018: Robo-advisors can answer questions. But do you know what to ask? - Aurora Tancock

Financial literacy is paramount

Financial literacy is paramount, given that individuals are increasingly expected to take on more personal responsibility for saving and investing for their retirement. Whether taking a do-it-yourself approach or relying on expert advice, a solid understanding of financial concepts will help people make better-informed decisions.

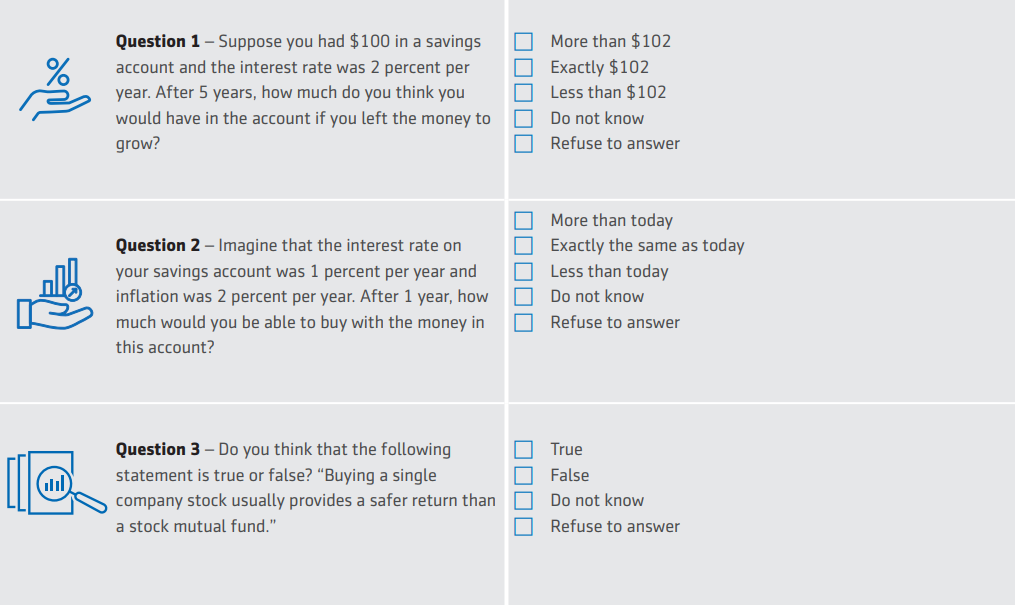

The survey uses a framework developed by Drs. Annamaria Lusardi and Olivia S. Mitchell dating back to 2004, to measure financial literacy. (Lusardi and Mitchell granted permission to ask the ‘Big Three’ financial literacy questions in the 2018 Aegon Retirement Readiness Survey. However they were not involved in the research.)

Lusardi and Mitchell created the ‘Big Three’ questions that measure understanding of compounding interest, inflation, and risk diversification. Their questions test actual knowledge of the topics, rather than self-reported knowledge. The questions are universal in nature and lend themselves well to language translation.

The "Big Three" financial literacy questions

Source: Aegon Retirement Readiness Survey 2018

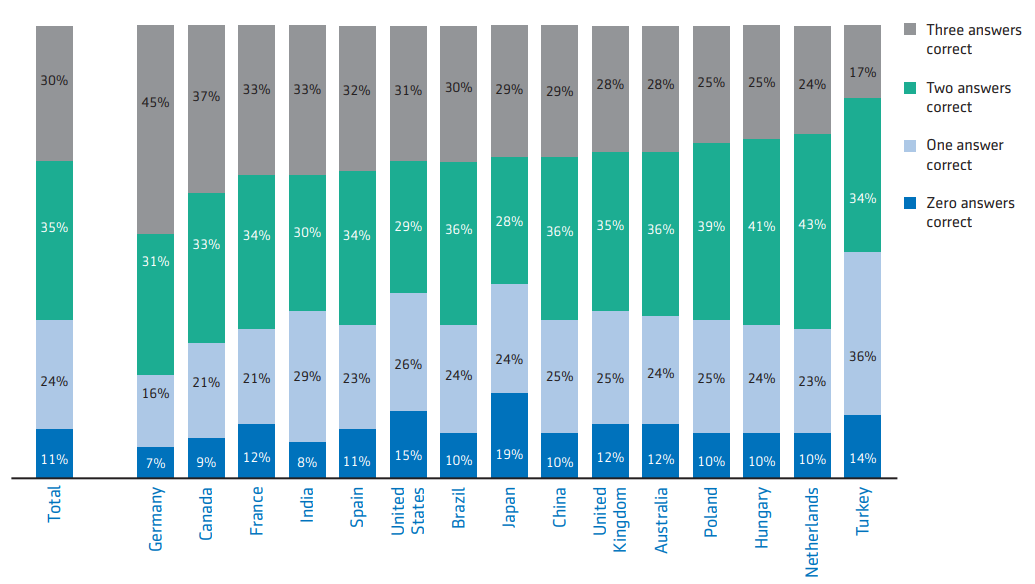

Low financial literacy around the world

The survey corroborates Lusardi and Mitchell’s research findings that financial literacy is low around the world.

Only 30% answer all "Big Three" questions correctly

Source: Aegon Retirement Readiness Survey 2018

Globally, the survey finds only 30% of respondents correctly answered all three questions. Financial literacy is highest in Germany, with 45% answering all three correctly, and lowest in Turkey (17%), for the countries considered. A concerning 11% of people globally did not answer any of the three questions correctly.

Read:

Do you have LGBT clients? They probably need more help in retirement planning because of "wage penalty"

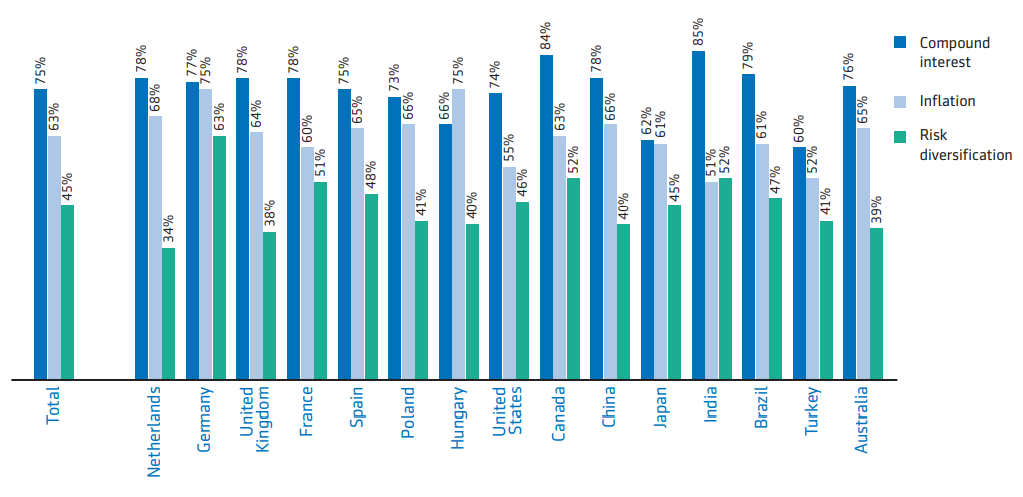

The correct responses are of course "More than $102", "Less than today", and "False".

Correct responses to the "Big Three" questions by topic

Source: Aegon Retirement Readiness Survey 2018

Without the requisite level of financial knowledge, it is impossible for people to formulate good retirement plans, or even know what questions to ask of advisers and retirement plan providers when seeking advice.

Low financial literacy may also translate into failure to engage in any kind of retirement planning.

In a world in which workers are expected to exercise more choice over how much they put aside for retirement, and how their retirement savings are invested, it is imperative to increase financial literacy among adults and to provide more education starting at an early age so that children can gain these vital skills that will serve them throughout their lives.

The lack of widespread financial literacy is alarming. Addressing it should be a top priority for policymakers, educators, retirement benefit providers and others.

The Aegon Retirement Readiness Survey was produced by The Aegon Center for Longevity and Retirement (ACLR), in collaboration with nonprofits the Transamerica Center for Retirement Studies, which is based in the US) and Instituto de Longevidade Mongeral Aegon, which is based in Brazil.

This year's report was based on the contributions from 14,400 workers and 1,600 retired people in 15 countries: Australia, Brazil, Canada, China, France, Germany, Hungary, India, Japan, the Netherlands, Poland, Spain, Turkey, the UK, and the US.

Connect with us on Facebook and subscribe to our weekly newsletter here.