In this article Simon Drimer, Managing Director of Pi Financial Services Intelligence, a specialist provider of insurance distribution channel market intelligence across Asia, examines the evidence on growth in agency force numbers and quality across the 12 major Asian markets (ex Japan): China, Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Sri Lanka, Taiwan, Thailand, and Vietnam over calendar year 2017.

Agency headcount

There were 13.3 million tied agents across these 12 markets on 31 December 2017, a significant increase from the previous year due mainly to the rise in headcount in China of 18% over the year.

Chinese agency headcount constitutes 70% of the total across the 12 markets, and India constitutes another 19% (about half of which is LIC). The two next largest agency forces are in Indonesia (535,000 - with Prudential UK about half of that number) and Vietnam (572,000 - with Prudential UK about one-third of that number).

The largest 12 company agency forces across Asia make up 71% of this total figure of 13.3 million agents, and eight of these companies are in China.

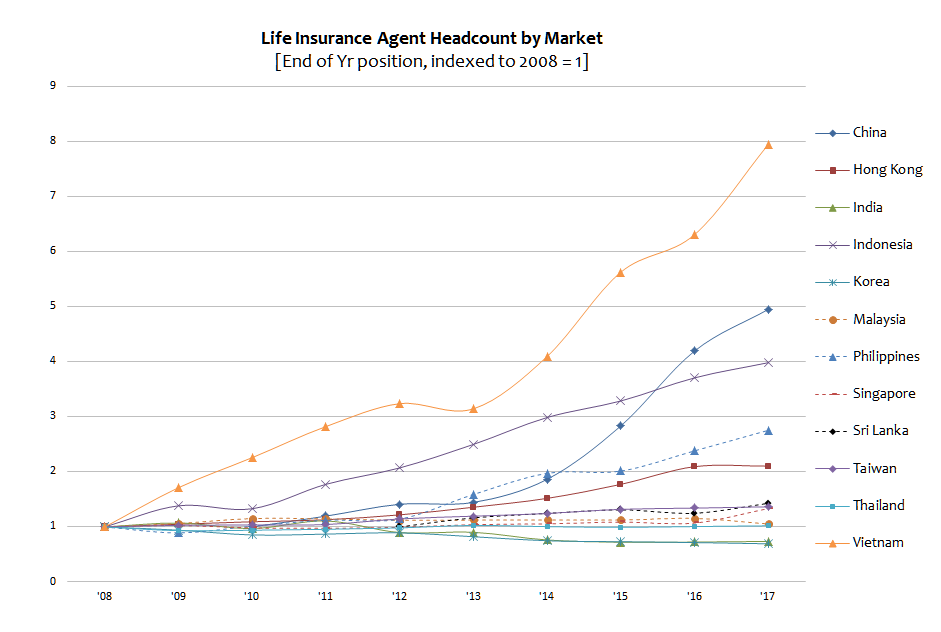

The first chart shows agent headcount growth from 2008 – 2017, indexed back to a common starting point on 31 December 2008.

Collectively, the 12 markets grew headcount strongly over the 12 months to 31 December 2017. However Chinese market growth was the main driver.

Looking at individual markets, we see that six of the markets were relatively flat, with mildly negative or mildly positive agent headcount growth: HK, India, Korea, Sri Lanka, Taiwan, and Thailand.

This is the first time in many years that the Hong Kong market was relatively flat, as Mainland Chinese Visitor business dropped off in 2017. Meanwhile, Malaysia was significantly negative: -9%, partly through transfers to the takaful agency system, which is excluded from our numbers.

How does your commission structure compare with fellow agents in other countries?

Growing headcount strongly were China (+18%), Indonesia (+7%), the Philippines (+15%), Singapore (+25% - mainly from the growth of life company affiliated IFA firms, which we include in our agency force headcount), and Vietnam (+26%).

Leaving aside the Chinese market, the implications for agents and agency channel managers is clear: agency distribution headcount growth cannot be relied on to deliver business growth. Growth must come from other channels, or else from improvements in agency force productivity and margins.

Interestingly, most of the multinationals in these markets – AIA, AXA, Ageas, Allianz, Aviva, Generali, Manulife, Metlife, Sun Life, and Tokio Marine – have not been growing headcount particularly strongly. There are a few exceptions: some of the new entrants to Vietnam and Indonesia, and most of the multinationals in China, have accelerated their growth over 2017. Otherwise, agent headcount gains have been modest for the multinationals in general.

Agency productivity

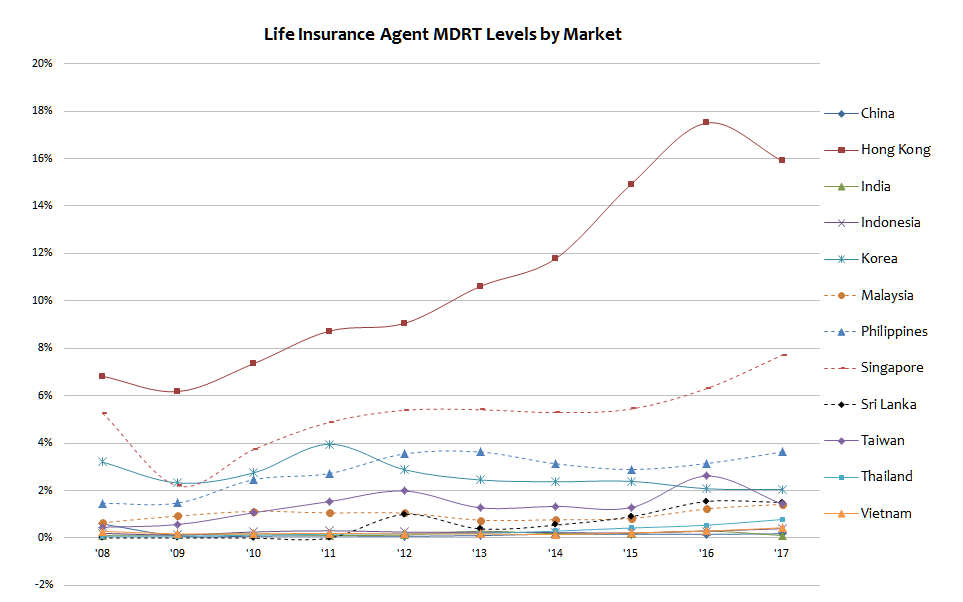

Has agency productivity improved over 2017? It’s difficult to measure across all markets, even at the market level, because while we have agency headcount and new business figures, we don’t have the proportion of new business by channel across all markets. In some markets like Hong Kong we know that agency productivity, even for multinationals, dropped over 2017.

But we do have a proxy measure for agency productivity, which gives us a common currency across all markets: MDRT membership as a percentage of the agency population.

We have been tracking these MDRT levels for nine years now, even at a company-by-company level, and this is the picture we see at the market level:

So this fairly crude measure of agency quality (and productivity), shows that in six markets over 2016-2017 there were increasing proportions of agents able to achieve the sales thresholds that give them MDRT membership: China, Indonesia, Malaysia, Singapore, Thailand and Vietnam.

Can adviser and online channels evolve to be demand-driven?

In all these six except for Singapore, though, the markets were coming off very low levels of MDRT penetration (and low levels of average agent productivity).

In three markets, MDRT levels over 2016-2017 were flat or slightly negative: Korea, Philippines, Sri Lanka. And in three markets there was a sharp drop-off in MDRT penetration levels: Hong Kong, India, and Taiwan.

We can conclude that only in China and Vietnam did we see the application of both levers of agency channel growth over 2017: agency headcount and agency quality. In all the other markets, one, or both of these levers were missing over 2017.

Connect with Asia Advisers Network on Facebook, Twitter and YouTube.