Although this is a US report, there are many lessons applicable to millennials in any part of the world.

With more than 90% of millennials owning a smartphone, you would think that the millennials who live in a world of technology would have a grasp of financial literacy as information is readily accessible online.

The smartphones provide their owners with a degree of convenience, allowing expenses to be tracked and online payments to be made. However, these fintech activities do not necessarily mean better financial management.

In the P-Fin Index report, those millennials who use mobile payments have a higher tendency to overdraw their checking account, and those who track their expenses via their smartphones are not doing better than those who do not.

Fintech users will only benefit if they’re able to make sound financial decisions. Being able to use technology to their advantage when it comes to finances will help boost their financial management.

It is important to pay attention to the millennials. After all, they made up 71 million of the population in the US in 2016. They are also expected to surpass the baby boomers as the largest generation in the US. Poking our noses into their financial affairs is crucial as the millennials’ personal finances would eventually become a big portion of the US economy in due time.

Believe the numbers

Only 11% of the millennials had smarts in financial knowledge when they answered over 75% of the questions asked correctly. While 28% of millennials demonstrated little financial knowledge when they answered less than 25% of the questions asked correctly. Overall, only 41% of millennials answered over one-half of the P-Fin Index questions correctly.

So what exactly does the P-Fin Index quizzes on?

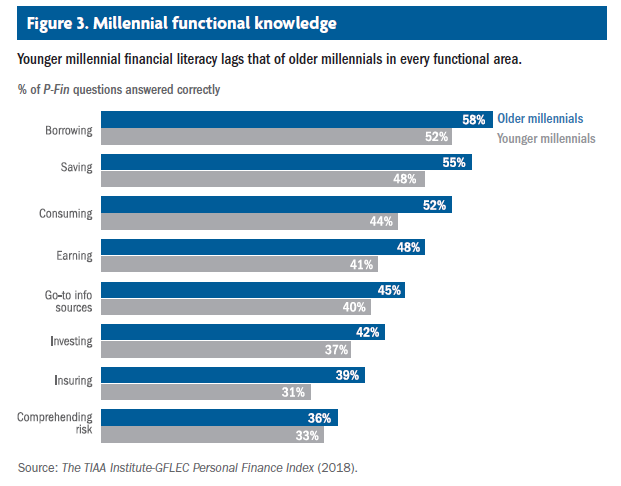

The P-Fin Index gauges personal finance knowledge and understanding in eight functional areas:

1. Earning—determinants of wages and take-home pay.

2. Consuming—budgets and managing spending.

3. Saving—factors that maximise accumulations.

4. Investing—investment types, risk and return.

5. Borrowing/managing debt—relationship between loan features and repayments.

6. Insuring—types of coverage and how insurance works.

7. Comprehending risk—understanding uncertain financial outcomes.

8. Go-to information sources—recognising appropriate sources and advice.

According to the survey, younger millennials’ (age 18 to 27) financial literacy lags that of older millennials (age 28 to 37) in every functional area.

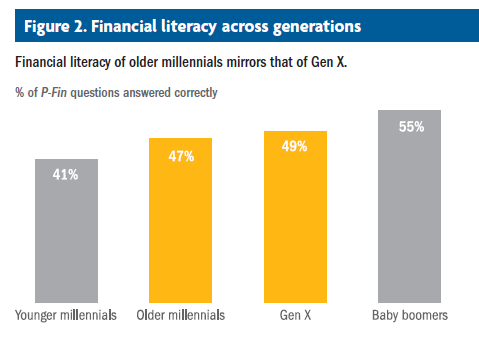

Here’s how the other age groups compare with one another:

You will notice that there is an increase in financial knowledge with age from the chart above. These findings are consistent with the results from other surveys. The conclusion is that, as people course through their life, they are met with various financial decisions to make, this in turns increase their level of financial literacy.

Managing personal finances with technology

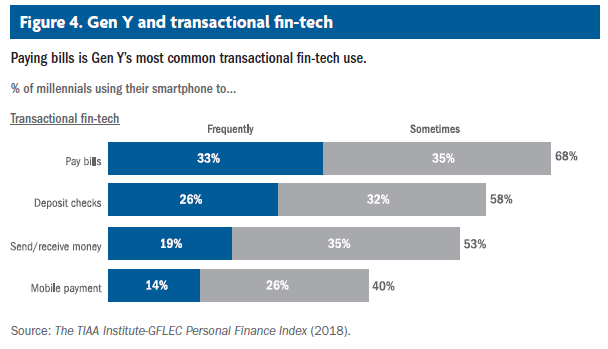

In the P-Fin Index, respondents with a smartphone were asked how frequently they use their device base on four transactional activities:

- Depositing checks into a bank account.

- Sending and/or receiving money from friends, family or other individuals.

- Paying for a product/ service in person at a store, gas station or restaurant using their phones.

- Paying bills.

The results: Paying bills is Gen Y’s most common transactional fintech use.

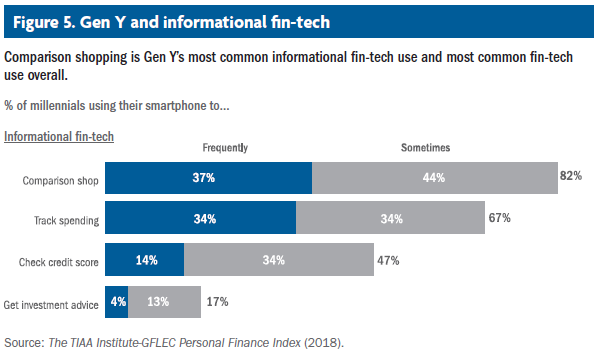

The survey also asked about smartphone use for four informational activities:

- Checking credit score.

- Comparing prices or product features when shopping.

- Getting personalised investment advice.

- Tracking spending.

From the charts above, it is clear that millennials use fintech to manage their personal finances. With 82% of them using their smartphones to compare prices or check out product features while they’re shopping.

Fintech as a double-edged sword?

To some, fintech is a useful and convenient tool. It has the potential to improve personal finance decisions and behaviour. Some fintech activities promote better personal finance outcomes, eg. tracking expenditure and making bill payments to avoid penalties.

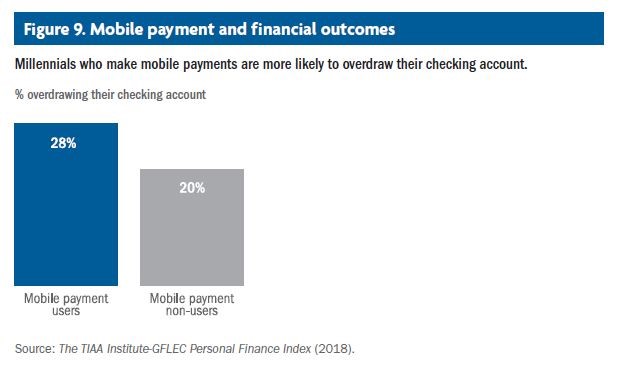

However, some fintech activities may result in poorer financial outcomes, eg. mobile payments for point-of-sale transactions. Left your wallet at home? Not an issue, all you need to do is to wave, tap your smartphone over a sensor at checkout, scan a barcode or QR code or use a mobile app while making payment.

Case in point, the convenience of using a smartphone for such transactions would cause users to overspend instead of helping them.

The charm of mobile payment apps such as Apple Pay, Google Pay and Samsung Pay is that they are easily accessible and swift in point-of-sale transactions. According to the FinTech report 2018 - Digital Payments by Statista Digital Market Outlook, mobile point-of-sale payments totalled over $70 billion in 2017 and are forecast to reach approximately $370 billion in 2022. The number of users is expected to grow from almost 50 million in 2017 to 90 million in 2022.

28% of millennials who use their smartphone to make mobile payments reported overdrawing their checking account. For the rest of the millennials who do not use their smartphones to make mobile payments, 20% do not need mobile payments to help them overspend.

What’s the take home?

There is no conclusion that deduces fintech to poor or good personal finance outcome. The findings, however, do report millennials as heavy users of fintech.

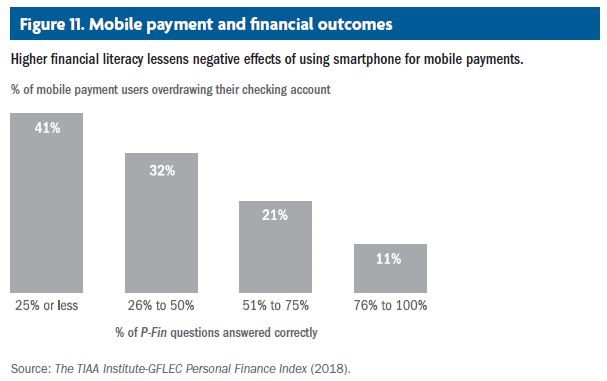

And millennials with higher levels of financial literacy still do overspend, but only a small fraction of them do. Millennials with the lowest financial literacy are the highest overspenders, with 41% of them overdrawing their checking account.

Research confirms that having high financial literacy does help one make appropriate decisions and experience better financial outcomes. Millennials who do not equip themselves with more financial knowledge would inevitably be exposed to risks and problematic financial situations as they progress in life.

Making decisions from a range of insurance choices would be difficult for millennials with lower financial literacy as they may not be insuring appropriate risks at appropriate levels or may not be doing so in a cost-effective way.

So get out there and help your clients to plan and get financially educated. Even if they look like tech-savvy millennials in the know.

Download the report here.

I can read your mind, you might like these, too:

It all starts with a dream - exclusive interview with an astronaut

Singapore:Number of centenarians has grown from 50 in 1990 to 1,100 in 2015 - Are you ready for 100?

Do you have a new product or programme to share? Or perhaps you are keen to explore any collaborations with us or our partners? Reach out to us at Connect@AsiaAdvisersNetwork.com