What will happen in the event of a winding up of a takaful operator (TO)? Here's the ruling of the Shariah Advisory Council (SAC) of Bank Negara Malaysia (BNM) at its 186th Meeting with immediate effect.

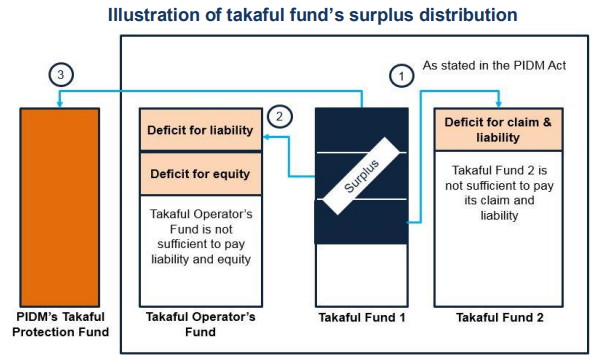

According to the BNM statement released on 9 October, the SAC at the meeting on 31 July 2018 decided that the distribution of a takaful fund’s surplus (after meeting all of the takaful participant’s rights and takaful fund’s liabilities) in the event of a winding up of a TO to the takaful protection fund managed and owned by Malaysia Deposit Insurance Corporation (PIDM) is permissible, provided that such surplus shall first be utilised to cover the deficit of any other takaful funds and the liability of the failed TO.

Background

- There was a proposal from PIDM to distribute the surplus of a takaful fund (managed by TO) in the event of winding up of a TO to the takaful protection fund owned and managed by PIDM.

- This proposal is intended to strengthen PIDM’s funds in order to exercise its mandate in providing protection against the loss of takaful benefits if a TO failed; and at the same time, to promote and contribute to the stability of the financial system.

Shariah Issue

Is the proposed takaful fund’s surplus distribution method Shariah compliant?

(Source: BNM)

Key Highlights of the SAC Discussion

Ownership status of takaful fund surplus (managed by TO) in the event of winding up of a TO

- The surplus is no longer owned by any takaful participant and TO. This is due to the fact that all takaful fund’s liabilities and participants’ rights have been fulfilled before such surplus is channelled to the takaful protection fund managed and owned by PIDM.

Mechanism to distribute takaful fund’s surplus to PIDM’s takaful protection fund

- There are two (2) types of takaful protection funds owned and managed by PIDM, namely the general takaful protection fund (GTPF) and family takaful protection fund (FTPF).

- The distribution of surplus either to GTPF or FTPF depends on the type of business of the failed TO, whether general takaful or family takaful business.

- Such distribution will only be executed after (i) meeting the takaful participants’ rights and takaful fund’s liabilities; and (ii) the surplus being utilised to cover the deficit of other takaful funds, as well as liability of the failed TO.

Utilisation purposes of PIDM’s takaful protection fund

- Among the main utilisation purposes of PIDM’s takaful protection fund are as follows:

- Payment of takaful benefits in the event of winding up of a TO;

- Resolution of a failed TO; and

- Payment for PIDM’s expenditure, including infrastructure development and human capital management in ensuring its readiness.

Permissibility for PIDM to utilise the takaful fund’s surplus for its expenditure purposes

- There is no Shariah prohibition for PIDM to utilise the takaful fund’s surplus for the purpose of its expenditure, provided that it brings benefits to the takaful sector as a whole and that it observes good governance practices.

Basis of Ruling

- The permissibility of proposed surplus distribution method in the event of winding up of a TO is based on the consideration of siyasah syar`iyyah in order to strengthen PIDM’s takaful protection fund.

This is important for PIDM to exercise its mandate in managing an effective takaful participants protection system, thereby contributing to the stability of the financial system. This is in line with the following Islamic legal maxim:

“Acts of those with authority over people shall take into account the public interest.”

- Moreover, the takaful fund’s surplus is no longer owned by any party including the takaful participants and TO. Hence, the authority or regulator may decide the appropriate distribution mechanism of such surplus, in line with the previous SAC ruling, as follows:

The SAC at its 114th meeting dated 28 July 2018 ruled that in the event of winding up of a TO, the surplus of participant risk fund (after meeting all liabilities and participant’s rights) may be utilised according to the following methods:

i) Assist other takaful funds that experience a deficit, even if it is not stated in the takaful contract.

ii) For other purposes as specified by the regulator i.e. Bank Negara Malaysia, which include assisting any TO in settling its debts or for charity purposes.

This is because such surplus is no longer owned by any participant. The ruler (regulator) therefore may decide the method of distribution with regard to the surplus.

Impact of the SAC Ruling

- This ruling promotes a more effective takaful participants protection system and at the same time contributes to the stability of the financial system at the national level.

- This SAC ruling is not only in line but also refines the existing SAC ruling (at the 114th SAC meeting on 28 July 2012) which allows for the surplus to be utilised to cover the deficit of other takaful funds and liability of the failed TO, as well as for other purposes outlined by the Bank.

This ruling is immediately effective by the issuance of this statement on Bank Negara Malaysia’s website.

Download the full PDF document from the 186th Meeting of the Shariah Advisory Council (SAC) of Bank Negara Malaysia here.