By all accounts, Mrs B was fit as a fiddle with no known medical conditions or family history. Hence, it came as a shock when she was informed by her doctor in March, at the age of 38, that she had breast cancer and it was already in the advanced stage – stage 4.

Emotional distress aside, it soon became obvious that the road to recovery would take time and cost a substantial sum.

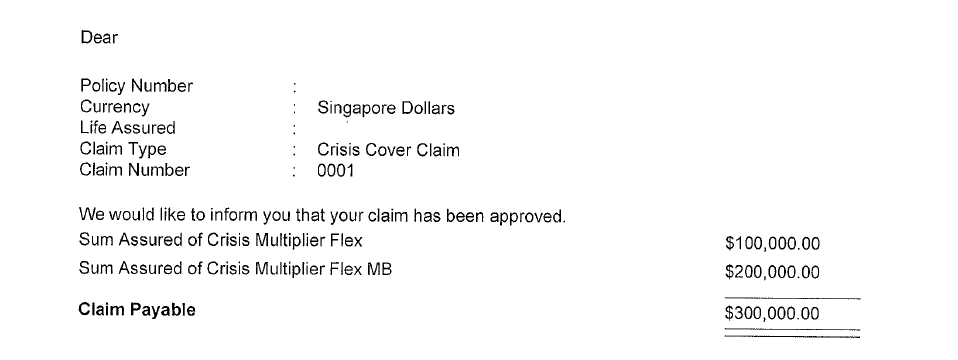

$214,000 for major treatments alone

Some of the major costs and treatments she has undergone are chemotherapy sessions from 2 May to 14 September costing S$160,000, surgery in October to remove the tumour costing $35,000, and radiotherapy sessions post-surgery from 2 November which lasted four weeks costing another $19,000. In addition, she is now undergoing a one-year antibodies treatment for her cancer.

(Above and main pic - some of the claims of Mrs B)

But thankfully, Mrs B has always been responsible and taken financial planning seriously. Her comprehensive hospitalisation insurance coverage and life insurance with sum assured of $700,000 have come in useful to ease her family from financial burden. It has allowed her to concentrate fully on her recovery journey.

“Without insurance, I wouldn’t know where to find the money for my cancer treatment,” she said.

“Some” is better than none

She bought her first insurance policy at the age of 24 right after graduation. On why she saw the need to do so, she said, “Insurance to me is really what the name suggests. It may happen, it may not happen. Hence, my philosophy is to buy some since you will never know when it will strike. It is like how some people will buy lottery even with the low odds for a chance to strike. Insurance to me is even more important, as it concerns financial security for my family.”

So it is puzzling why some people choose to spend money on lottery but refuse to buy insurance, she added.

Professionalism matters

She also counts it a blessing to have met Eric Seah Sheau Ming, a financial consultant representing a leading UK insurer.

(Pic: Mr Eric Seah with client)

“I met Eric, who was introduced to me by my sister. I had little knowledge of insurance or financial planning. I also had little savings and a low budget since I had just started working. But I remember Eric being patient and professional, nonetheless. He didn’t just try to sell me a product, and he wasn’t pushy,” she said.

She said that Eric took time to obtain her financial profile and understand her financial goals and objectives. Thereafter, he explained the various savings and risk management ratios she should be aiming for based on her profile and the gaps she had before proposing and explaining the various options.

“Eric’s professionalism put me at ease and earned my trust. We are always faced with competing priorities and limited budget. His systematic approach meant that I had a clear roadmap in mind. Over the years, every time I meet Eric, he would follow the same systematic approach, and we progressively filled the gaps,” she said.

It’s a responsibility

As for Eric Seah, he said the role of a financial consultant is more than a job. It’s a responsibility.

“When clients place their trust in us, they are putting their financial security in our hands. It is our responsibility to do our best and work with our clients to ensure that they are financially protected,” he said.

Hence, it is also important for advisers to continue to upgrade their level of skills and expertise, said Eric who holds the Chartered Financial Planner (CFP), Chartered Financial Consultant (ChFC) and Associate Estate Planning Practitioner (AEPP) qualifications. As an Agency Leader, Eric is a Chartered Insurance Agency Manager (CIAM) and Certified Manager of Financial Advisors (CMFA) awarded by Life Insurance and Market Research Association (LIMRA)

And after close to 25 years in the industry, he continues to be passionate about what he does as seeing insurance in action and how it has helped his clients in times of need have further strengthened his belief in the profession.

“It is understandable that some people may not understand or is even sceptical about the role we – financial consultants – play. But as practitioners, we must continue to be true professionals to change the image of the industry,” he said.

Financial planning requires a systematic approach and is a continuous process to take into account changes in a client’s life stages. It cannot be a one-time sale. “We can’t control whether a client does anything, but we must control that we diligently conduct annual reviews with our clients to keep them updated and remind them of any shortfalls.”

Annual review

On the same note, he highlighted that clients should also be open to meeting their advisers for reviews.

“Don’t be afraid of meeting your adviser thinking that we are out to push you to buy something. It is important to do a financial review at least once a year with your adviser so we can be aware of the situation you are in, whether the strategic roadmap needs to change and the various options available to do so. You have every right to decide whether or not to accept our proposals depending on your priorities, circumstances and budget. But do it from the point of knowledge.”

Referring to the experience of Mrs B, Eric said, “If I had done a one-time sale and disappeared back when she graduated, or if she had not continued to meet me for annual reviews, she would not have anywhere close to the coverage and protection we managed to secure for her over the years. Some years she enhanced her coverage, some years she didn’t, but we always had a clear roadmap of where we are at and where we are going. And I take pride in knowing that what I do has helped to at least ease her financial burden in this trying time so she can concentrate on getting well.”

The 4 main levels of financial planning**

1. Risk Management

- Minimum 5-10 times of annual income against premature death and disability

- Minimum 3-5 times of annual income against critical illness

- Comprehensive hospitalisation coverage

- Personal accident coverage

2. Wealth Accumulation

- Retirement planning needs

- Children’s education planning needs

3. Wealth Preservation

- Tax planning through tools including Supplementary Retirement Scheme (SRS)

- Topping up of parent’s CPF (Central Provident Fund)

4. Wealth Distribution

- Wealth distribution through wills, trust, beneficiaries’ nominations, CPF nomination, Lasting Power of Attorney (LPA) and Advance Medical Directive.

Eric is also active in contributing to the insurance industry. He has served in the executive committee of Financial Services Manager Association Singapore (FSMA) for six years, holding various appointments including education chairman, treasurer and honorary secretary. He is also a moderator for Agency Management Training Course (AMTC) Classes offered by FSMA.

** Please note that these are general rules of thumbs and simplified for this article

* Mrs B declined to be named for privacy reasons

Read also:

Insurance adviser to the rescue - Successful critical illness claim after four years

Position yourself for success - Insurance Agent of the Year Amy Wat

No evidence yet that tech firms can disrupt life insurance sector - AIA Group Chief Executive

Follow Asia Advisers Network Facebook page and sign up for our complimentary weekly newsletter.