Despite the hype around direct digital distribution, the defining evidence so far points to a lack of demand and a gap between actual adoption and the stated use of online direct for purchasing life insurance.

In this article, Nick Li, a Principal at NMG Consulting based in Singapore, shares his thoughts on how adviser and online direct channels will evolve:

Long-term macro trends such as increasing smartphone penetration, better use of data and analytics and demographic changes will support a shift from traditional face-to-face to online direct channels for the distribution of life insurance. These macro trends are more likely to be the facilitators of digital purchase, not the impetus.

Similarly, regulatory support such as Direct Purchase Insurance in Singapore, Direct Distribution Channels in Malaysia and various regulatory sandboxes aimed at digitalising life insurance are enablers for digital rather than the underlying motivators.

Need does not translate directly to demand

The success of direct digital distribution relies on both demand and supply factors, but the defining evidence so far points to a lack of demand, with the widely available online direct channel generating low life insurance volumes.

Furthermore, there is a misconception that need equates to demand. The widely reported protection gap in Asia indicates a clear need, but that will not translate into demand without an increase in insurance awareness and education.

Life insurance remains sold rather than bought

There are intrinsic and execution factors as to why life insurance remains a sold rather than bought product.

With respect to intrinsic factors, face-to-face interaction and quality advice are valued, particularly for long-term contracts. Customers appreciate the comfort of knowing a real person will be available to answer questions about their policy or assist with a claim several years down the track.

In addition, life insurance education and awareness are generally low in Asia and products relatively complicated and hard to understand, making trusted advice highly valuable.

With respect to execution factors, there is a gap between actual adoption and the stated use of online direct for purchasing life insurance.

NMG research shows that each year a small proportion of customers indicate that they purchased life insurance online, although a significantly larger proportion indicate that they intend to use online channels in future.

This has been a consistent trend observed over the past several years. One possible explanation for this persistent gap is that the idea of online life insurance is attractive to many, but when it comes to the actual purchase, the practical challenges of understanding the products on offer and filling in online questionnaires cause customers to revert to face-to-face interactions.

Although customers are not in the main purchasing online, there is evidence that they are using it for research. In addition, customers, especially millennials, value an omni-channel experience – traditional face-to-face advice combined with online/digital tools, and this could be the foundation of future purchasing behaviour.

Adviser and online direct channels will evolve to their natural customer bases

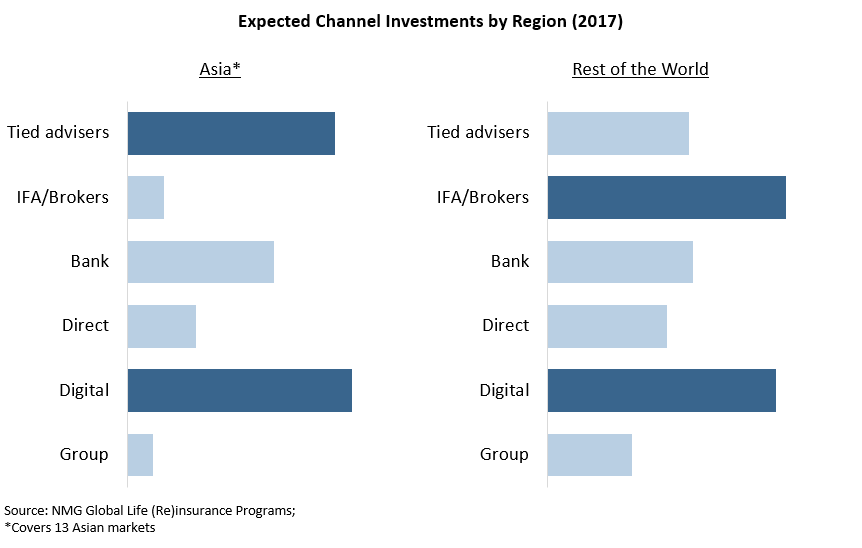

Insurers are continuing to invest in adviser and digital channels globally. NMG research across 13 Asian markets shows that in aggregate, Asian insurers intend to continue to invest significantly in agency and digital channels over the next 3 to 5 years.

Chart – Proportion of insurers expecting to invest in channel over the next 3 – 5 years (2017)

The mass market, part-timer agency model and the online channel currently target a similar customer base in Asia. It is a reasonable expectation however that the segregation of roles between the adviser and online channels will become increasingly apparent in future.

The adviser channel will respond by:

- Increasing its level of professionalism. This will be led by a push from regulators in Asia, in the form of potential minimum education and increased disclosure requirements being imposed medium to long term, following similar discussions taking place currently in more mature markets;

- Shifting its target customer base from mass market towards more mass affluent and above, who are time-poor and have more financially complex needs. These segments will more likely require advice;

- Continuing to dominate sales of complex products, such as those requiring more explanation; and

- Retaining its dominance of complex underwriting cases. For example, on sub-standard lives and customers with prior illnesses where underwriting is more complex and a deeper understanding of product and product features is required.

Adviser models will continue to evolve. The market has seen the Financial Adviser channel evolve in Singapore over the last few years, and insurers piloting or looking to pilot salaried/professional agencies throughout Asia. These models will support the industry in moving from a mass market, part-timer sales force to a more professional, capabilities-based model.

The online channel will also become more distinct, by:

- Continuing to focus on simple products such as standalone term life, TPD, critical illness, accident and health insurance, which are relatively easy for customers to understand;

- Concentrating on the mass market. Online will appeal to customer segments which value speed and convenience, have relatively simple needs and are potentially more price sensitive. As mentioned earlier, the next hurdle for success in online distribution will need to be overcome by demand. The challenge is to increase customers’ insurance awareness, education and wealth levels; and

- Focusing on younger, more digital savvy customers as they have greater trust in the online channel.

The model for online distribution will also evolve. The evidence points to the key area of focus shifting away from online direct and being replaced by digital affinity partnerships and digital support.

Life insurers are already investigating how they can use affinity partners’ data and distribution access to provide more relevant offers, improve conversion rates, improve customer experience and lower acquisition costs. Post the experience of ‘going at it alone’ in digital, they now seek to realise the benefits of being embedded in an ecosystem.

The final word

Can life insurance distribution become demand driven in the future? The demand for life insurance will increase over time greater insurance education and awareness, as well as general wealth increases across Asia.

However, this will be a long process requiring effort from all market participants. Throughout this process and ultimately, advisers and online channels will evolve to better meet the needs of their natural customer bases, and that can only help.

Read also:

No robot is going to take your place - AIA Group Chief Marketing Officer

Distribution channels need to evolve - MD of Max Life Insurance