COVID-19 has turned the world upside down, with the global economy going into reverse and countries shutting down across the world. China was the first country to shut down and is one of the first to reopen. Today, many industries, including insurance, are watching closely to see what happens as China progresses through its economic recovery. Arthur Bi and David Schiff, Partners at McKinsey, share their insights in this article.

According to the latest findings from McKinsey’s consumer surveys, overall economic sentiment in China is positive, and the most recent spending and traffic data suggest that the economy has started to rebound.

While the broad economic view in China may look good, the outlook for the insurance industry is complex – some areas experienced growth and others declined.

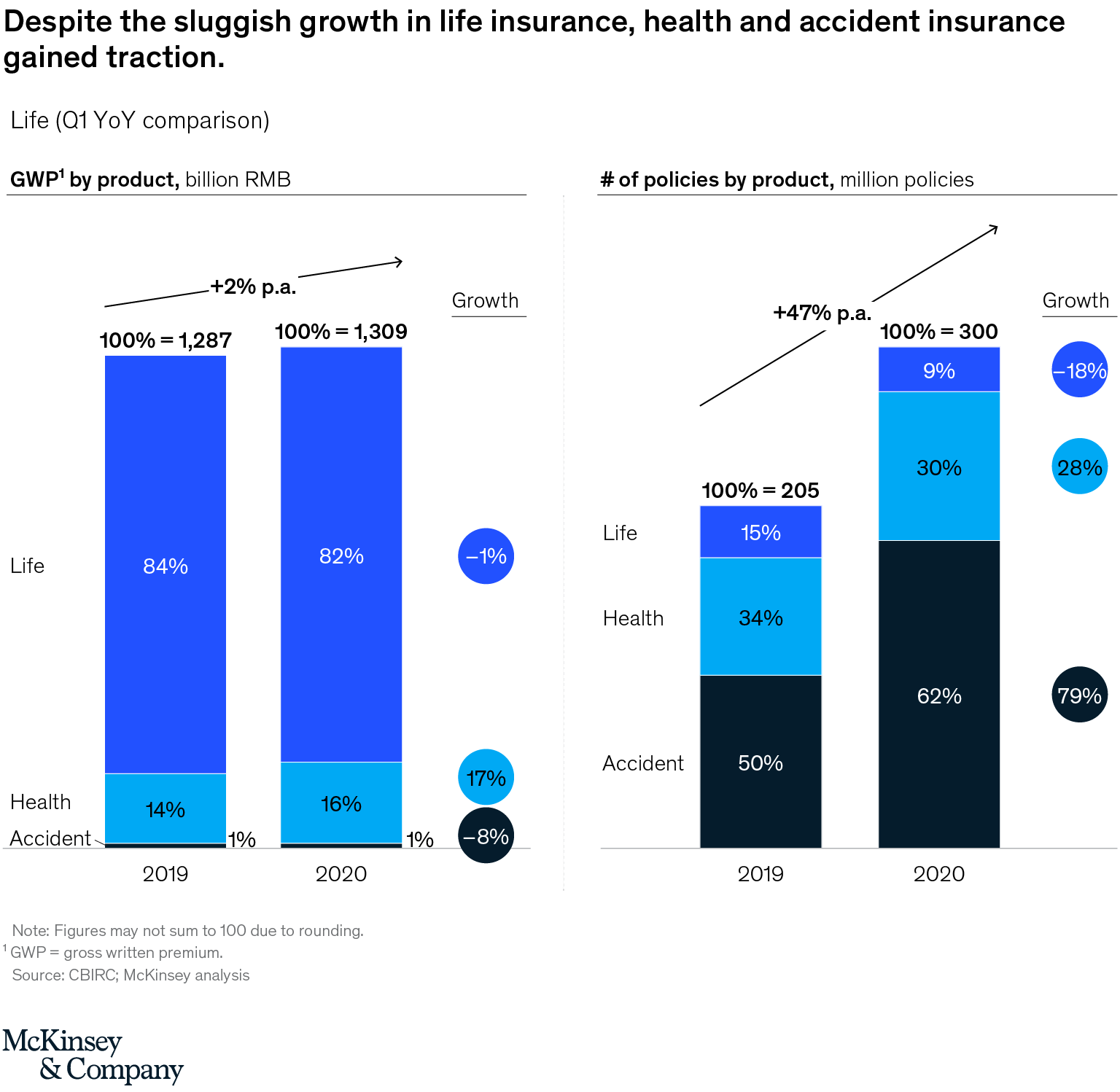

For example, health insurance sales grew by an impressive 17 per cent between Q1 2019 and Q1 2020, while life insurance sales retracted by 1 per cent over the same period. Also, the demand for auto and liabilities policies slowed significantly.

As insurers outside China continue to weather the COVID-19 crisis and prepare for a possible second or third wave, Chinese insurers are setting an example of how to endure the storm and emerge from the crisis stronger.

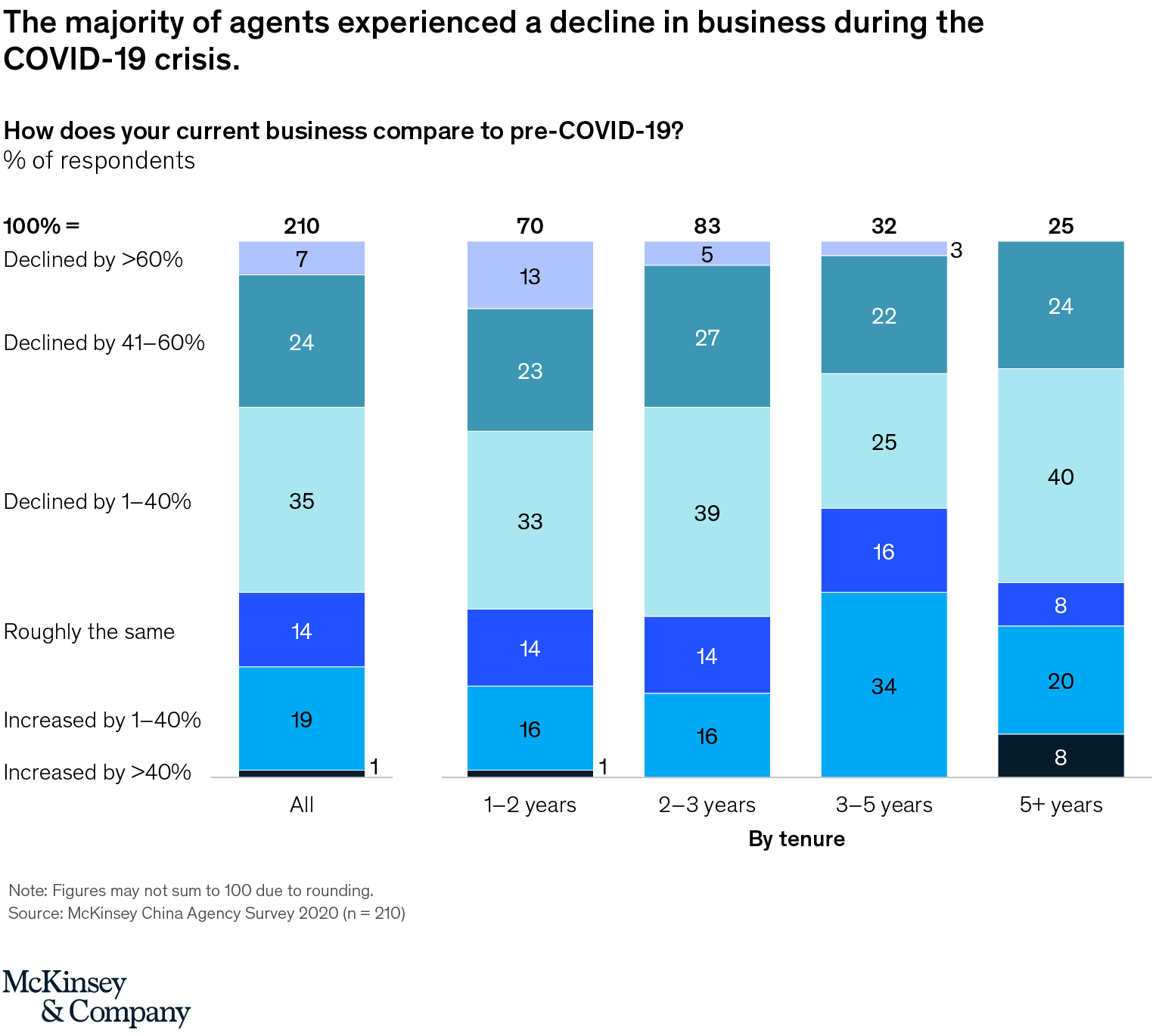

We surveyed over 200 agents in China across all areas of the insurance industry in April 2020 to gauge their sentiment, performance and future outlook.

How COVID-19 has affected agents

Despite being one of the hardest-hit industries, many agents are optimistic about the future and rising to the significant challenges they face on the road ahead.

Since the pandemic took hold earlier this year, around two-thirds of agents experienced a sudden decline in business, while around 20 per cent reported an improvement.

However, overall, agents are optimistic about their future performance, with over 65 per cent of agents surveyed stating that their customers have become more proactive in inquiring about insurance products and shown stronger interest in health, accident and critical illness products, as well as online medical services.

With the shift away from in-person to digital interactions, it is no surprise that more than 60 per cent of agents stated that they are increasingly interacting with both prospective and existing customers over the phone. WeChat and video calls have also increased, with 53 per cent of agents using these tools more with existing customers. Sixty-one per cent said they are using these tools more frequently to interact with prospective customers.

Read also: Innovation at Ping An and the NextWave of insurance - EY Global Insurance Knowledge Leader

Thus, the importance of digital is clear, and the nimbler digital players who were less impacted by the crisis compared to their more traditional peers are now reaping the rewards. For example, digital insurer WeSure added more than 25 million active users to their platform during the pandemic.

To help agents deal with the new surge in customer demand and digital interactions, there are several steps that insurance companies can take, which many Chinese insurers have already made to help their agent networks.

Embrace the hybrid digital agency model

This new distribution model means agents could work with a full set of digital capabilities that enable seamless interactions with customers across channels. Insurers could provide agents with enhanced remote-working capabilities, so they can meet customer-protection needs virtually.

For example, they could enhance dynamic digital tools with product illustrations (that is, illustrations or icons that help users navigate a product and tap into its full value), as well as screen-sharing and videoconferencing to foster better communication between agents and customers. That said, insurers will need to continue to meet all regulatory requirements, including identity verification and signature collection.

Invest in digital tools and advanced analytics

The COVID-19 crisis has accelerated insurers’ investments in digital capabilities at a record rate. To help agents create their own digital journeys, insurers should provide them with digital platforms that allow customers’ needs to be assessed and applications submitted remotely, making the application process extremely convenient and seamless.

In the public domain, social media platforms can also be utilised to create community groups where agents can share marketing content with current and prospective clients. These investments will help agents prepare for a possible second wave of infections and potentially reduce business disruption.

Read this: Hong Kong: More 'Smart Consumer' Than 'Smart Investor' Amid COVID-19 Pandemic

Further, we have observed that these tools result in large efficiency gains for insurers (that is, a reduction in overall costs for the organisation), by allowing agents to spend more time with customers and less time completing administrative tasks.

On the advanced analytics side, models can be developed that allow agents to be matched with customers more accurately based on personality type, demographics, or profession, creating a more personalised and tailored customer experience. Also, analytics can be leveraged to assess and identify the best-performing agents within an insurer’s network.

Exploring new products and services

Consumers are proactively asking for help to bridge their protection gaps. Insurers need to embrace agile product development and ensure they are addressing the broadest range of consumer needs, while arming their agents with tools to provide those products via digital channels.

Value-added and non-policy services, such as remote health advisory and diagnosis, could be powerful new offerings for agents to have in their arsenal.

The COVID-19 pandemic has been a catalyst for insurers to accelerate digital transformations and improve customer-centricity. As insurers and agents around the world navigate the crisis and move into recovery, they can turn to China for insights.

One thing is clear: insurers will need to change how they support agents to help them become more resilient in the face of the pandemic and prepare for the new economy that will emerge.

About the authors

Arthur Bi is a partner in McKinsey’s Beijing office.

David Schiff is a partner in McKinsey’s Hong Kong office.

Check these out:

Building Trust Is Essential In Financial Advisory. Here's How.

An Attitude of Gratitude - Nick Vujicic

#MDRTDAYSG2020

More than 20,000 views of the 3-day Insurance Inspired Summit

P.S: Subscribe to Asia Advisers Network YouTube Channel