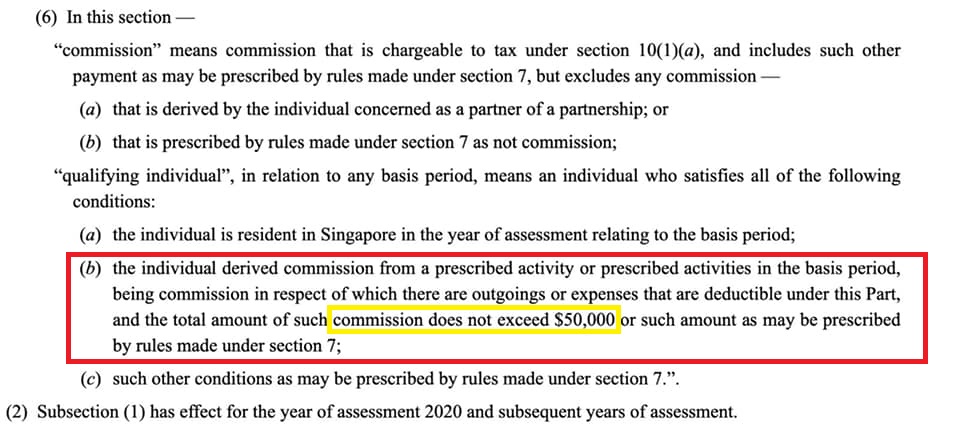

In the latest release of amendments for the Income Tax Act by the Ministry of Finance, Singapore, a new section is added in the principal Act concerning insurance agents earning commissions not exceeding $50,000.

These new Rules come into operation on 2nd Dec 2019.

For insurance agents who fall within this income bracket, they are allowed to opt-in for a percentage of their income to be deducted as expense even without supporting documents.

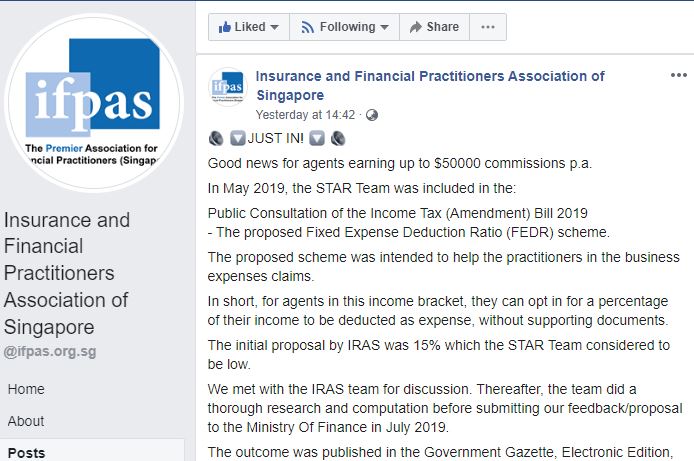

First hearing this news straight from IFPAS. We would like to commend the hard work of the STAR Team, without them the current proposal would be a low 15%. Their dedication led them to meet up with the IRAS team to give feedback and advocate for the industry.

As a friend of the insurance industry, we salute the associations and industry leaders who step up to serve and are always keeping a lookout for their fellow practitioners.

You can read the full post here:

Good news for agents earning up to $50000 commissions p.a.

In May 2019, the STAR Team was included in the:

Public Consultation of the Income Tax (Amendment) Bill 2019

- The proposed Fixed Expense Deduction Ratio (FEDR) scheme.

The proposed scheme was intended to help the practitioners in the business expenses claims.

In short, for agents in this income bracket, they can opt in for a percentage of their income to be deducted as expense, without supporting documents.

The initial proposal by IRAS was 15% which the STAR Team considered to be low.

We met with the IRAS team for discussion. Thereafter, the team did a thorough research and computation before submitting our feedback/proposal to the Ministry Of Finance in July 2019.

The outcome was published in the Government Gazette, Electronic Edition, on 2 December 2019 at 5 pm (below). The limit has been raised to 25%! This is good news indeed.

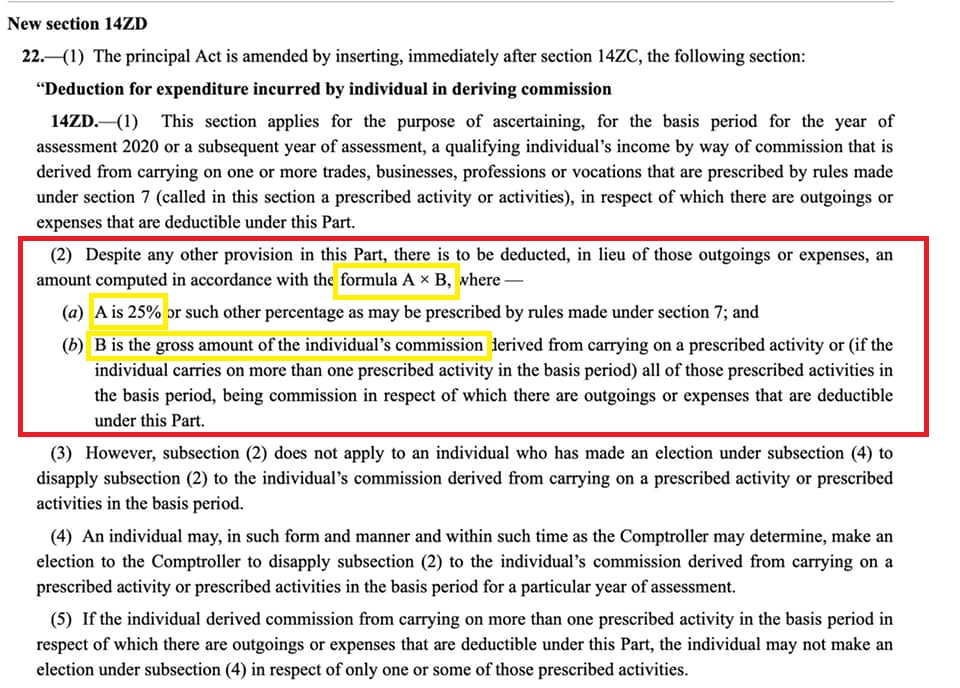

You can read the details: Income Tax Act Section 14ZD (below)

My team also proposed similar limits for higher income bands but they were not included in this outcome. Perhaps at a more opportune time, we will resume this conversation with them.

Meanwhile, have a blessed Christmas everyone!

Leong Sow Hoe

Dennis Tan

RolandYeo

Chan Keng Leong

Frank Ng

Michael Seow

For the full section of 14ZD of the Income Tax Act Section, see below: