The distribution function is a vital element of the insurance value chain, reflecting the fact that insurance is generally sold, rather than bought. Over time, face-to-face selling through agents and brokers became the dominant paradigm of distribution.

However, with the ubiquitous use of the Internet, coupled with customer preference for and expectation of convenience, digital elements increasingly permeate traditional distribution channels or even create new channels in their own right.

Against this backdrop, policymakers, regulators and corporate decision-makers alike explore the potential of these technology-induced trends to narrow persistent protection gaps, ranging from natural disaster risk to mortality and longevity risk protection.

In order to better understand the root causes of these protection gaps, The Geneva Association commissioned a survey of 7,000 customers in seven mature insurance markets to identify the main barriers to purchasing (life) insurance. The seven markets covered were the U.S., Japan, France, Germany, Italy, the U.K. and Switzerland.

An in-depth analysis of the drivers of customers’ life insurance buying decisions unearths three major determinants:

- behavioural biases,

- economic constraints or considerations, and

- a lack of knowledge.

Striking lack of life insurance awareness

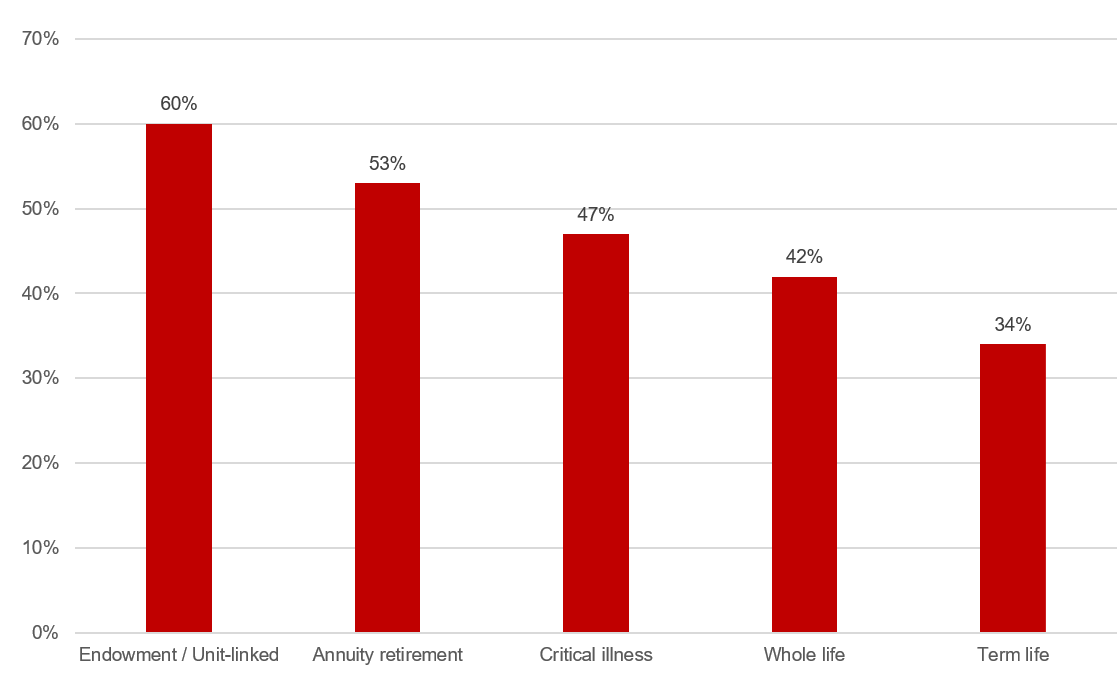

The survey also reveals a striking lack of life insurance awareness among respondents (Figure 1).

Looking at the average across all countries covered by the survey, the lowest levels of awareness relate to endowment and unit-linked insurance. Well over half (60%) of respondents were not aware of these products, which, unlike term life insurance, accumulate cash and pay a lump sum to beneficiaries upon the insured's death or back to the living policyholder when the policy's term matures.

The second least known product is annuity insurance, which in some countries is virtually non-existent. Over half (53%) of respondents were unaware of these financial products, which pay out a fixed stream of payments to an individual, typically during retirement.

Awareness is also low for critical illness cover, which pays a lump sum to the policyholder if s/he is diagnosed with an illness specified on a predetermined list. Almost half (47%) of survey respondents have never heard of critical illness insurance.

Not surprisingly, term life insurance stands out in terms of awareness. Two-thirds of respondents had heard of these relatively simple products, which offer guaranteed death benefits but, as opposed to endowment, unit-linked or whole life products, do not have a savings component.

Figure 1: Share of respondents who are not aware of the product

Source: Geneva Association Customer Survey

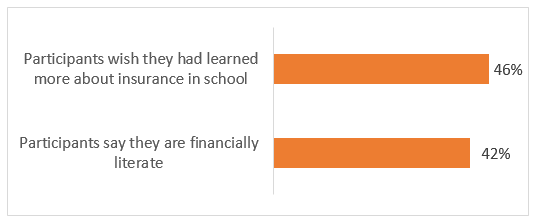

More generally, just 42% of respondents consider themselves financially literate and an even higher share regrets deficits in financial literacy (Figure 2).

This perception points to the potential of additional financial education and awareness building measures to spur demand for insurance.

Figure 2: Scope for insurers to educate customers (based on all respondents, percentage of those agreeing)

Source: Geneva Association Customer Survey

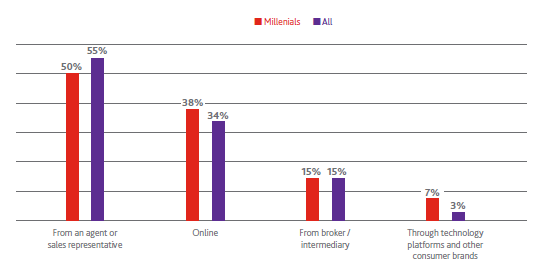

Preferred channel of distribution

These awareness and knowledge gaps revealed by Figures 1 and 2 may help understand why customers in mature economies prefer omni-channel distribution.

The agency channel is here to stay as 55% of the interviewees prefer to purchase insurance through it.

Interestingly, even 50% of the millennials interviewed prefer to buy insurance through an agent. The online channel ranks second. It is also noteworthy that only 3% of interviewees prefer to buy insurance through consumer brands and platforms. At 7%, the respective millennial share is equally insignificant.

This outcome invites a comparison with other sources (e.g. Capgemini/Efma, World Insurance Report 2018), according to which up to one-third of insurance customers in mature markets would consider buying insurance through technology platforms.

Obviously, there is a massive gap between the stated willingness to consider new avenues on the one hand and actual preferences on the other.

Figure 3: Preferred channel of distribution (in percent, based on all respondents)

Source: Geneva Association Customer Survey

Therefore, the digitalization of the agency force is arguably the core of any future-proof distribution strategy. Insurers need to build an omni-channel proposition to meet today’s and tomorrow’s customer buying preferences.

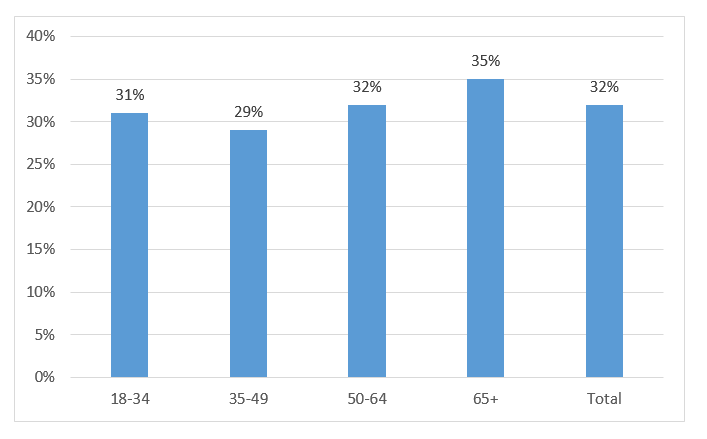

The key to customer trust

However, the actual role of the agency and any other distribution channel will remain a function of customer trust. It is intuitively plausible that those individuals and organisations at the frontline of the customer interface are critically important to the reputation and the level of trust placed in the ultimate insurance carrier.

In this context, the Geneva Association Customer Survey reveals major shortcomings in trust in insurance agents, with less than a third of respondents considering them trustworthy.

Several studies show empirically how a sales agent’s behaviour can build or deplete both customer trust in the salesperson and in the insurance company.

This research demonstrates that the agent’s ethical sales behaviour is crucial to winning customer loyalty through customer trust. Therefore, for the insurance industry, any effective strategy to rebuild trust must encompass those who are ultimately closest to the customer and their needs and concerns.

Figure 4: Percentage of those considering agents trustworthy

Source: Geneva Association Customer Survey

The future is hybrid

The bottom-line: The life insurance distribution landscape will remain more colourful than some pundits suggest.

Nothing points to the demise of the agency channel.

In the presence of massive knowledge gaps, customers continue to rely on trustworthy expert intermediaries.

It goes without saying that the digitalization of the agency channel is a necessary condition for its future relevance. The sufficient condition, however, is customer trust, the lubricant for insurance purchasing since the industry’s earliest days.

Dr Kai-Uwe Schanz was appointed Deputy Managing Director and Head of Research & Foresight of The Geneva Association in November 2019. In this role he is also the Secretary to the Global Reinsurance Forum (GRF).

Before joining The Geneva Association, Kai spent 12 years co-running a reinsurance-focused strategy, business development and communications consultancy, which he co-founded in 2007. During those 12 years, he served as an external advisor to The Geneva Association. From 2016 to 2018, he was a non-executive member of the Board of Directors of Trust International Insurance and Reinsurance Company headquartered in Bahrain.

Check these out, too:

AIA and EY reports 90% of HNWIs in Singapore leverage on insurance for their wealth and legacy planning

Grow your Legacy with the PreceptsGroup

Marketing during lockdown - 3 ways to reach your customers

Get your message across to over 30,000 fans and followers of Asia Advisers Network. Get in touch today to find out more. email: Connect@AsiaAdvisersNetwork.com