The Covid-19 outbreak has disrupted the traditional insurance agency model. While countries have begun to relax physical distancing requirements with the increasing rollout of vaccines, the pandemic's effects on the insurance agency model are likely to last for some time. However, there is light at the end of the tunnel, and it is prime time for the insurance industry to look beyond the pandemic and progress ahead of recovery and into the future. Bernhard Kotanko and Enoch Chan, Partners at McKinsey, share their insights in this article.

The outbreak has accelerated movement toward a digitally enabled hybrid model of distribution, in which agents are supplemented by a full set of digital capabilities enabling them to interact with customers via a seamless omnichannel journey. The move toward this new operating model will require Asian insurers to make significant changes to how they currently operate. Doing so successfully, however, could allow customers as well as agents and insurers to reap benefits. Customers could have an improved purchasing experience through omnichannel services, while agents could gain better insights into customer behaviour and tailor products and services accordingly.

To build a digitally enabled hybrid model successfully beyond the pandemic, agents should consider focusing on the following priorities.

Create a seamless omnichannel journey with contextual memory

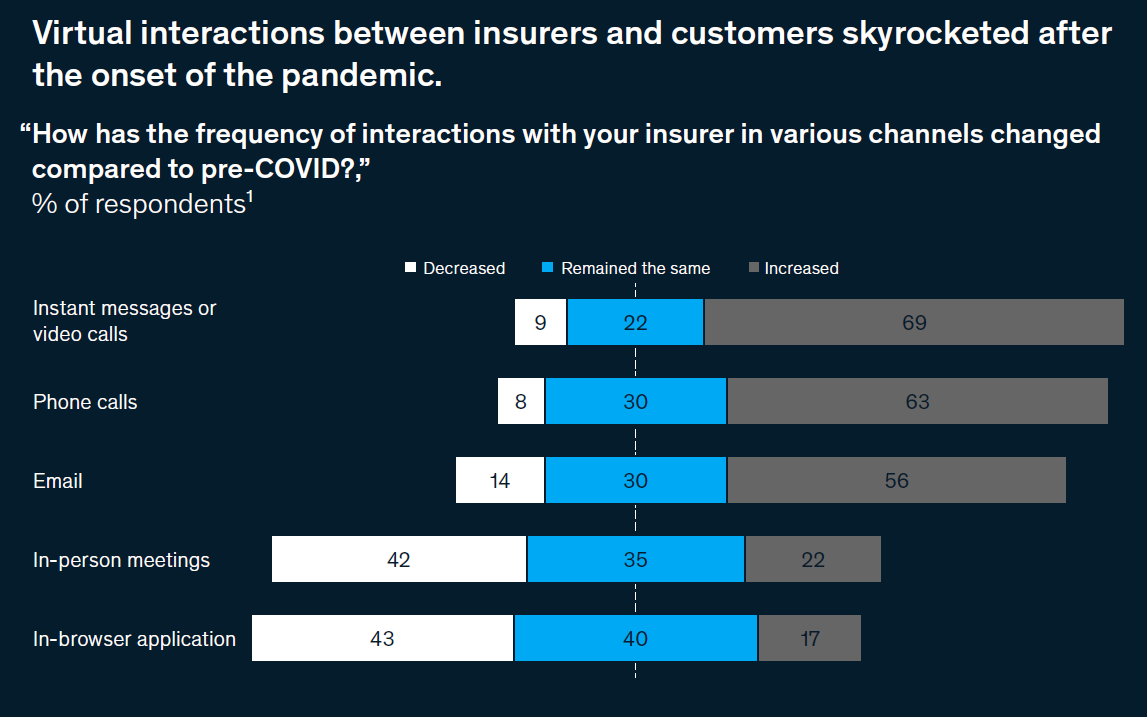

Infographics by McKinsey

Asian customers are increasingly accustomed to omnichannel experiences in their everyday life, with the emergence of new collaboration models between e-commerce and physical outlets. They expect the same seamless experience in their interactions with insurers. Insurers can start to create an optimal customer experience by identifying key touchpoints along the purchasing journey. These should be based on customer personas and contextual targeting to help create unique, tailored experiences at on- and offline points of contact.

The handover of information between agents and digital channels, such as during the transition from customer acquisition to customer advising, are particularly important. Handing it over seamlessly could prevent customers from being asked to provide information more than once during their journey.

Create affinity-building products

Traditionally, insurance companies spend more than 50 percent of new premiums on customer acquisition via agent commission and overrides. More and more insurers are exploring digital partnerships as a way to acquire customers. A leading Southeast Asian insurer, for example, has partnered with a ride-hailing start-up to launch the region’s first micro-insurance for critical-illness protection that is exclusively for drivers. This plan provides drivers with a flexible pay-per-trip and allows them to accumulate insurance coverage with each trip they complete.

Read this: Hong Kong: More 'Smart Consumer' Than 'Smart Investor' Amid COVID-19 Pandemic

Tailor offering to life moments

In a 2019 McKinsey survey of Chinese insurance customers, 85 percent of respondents said that they feel like agents are “always trying to sell products.” This highlights an area of opportunity, because less-experienced agents often struggle to learn about the life moments when customers might have a potential need for insurance products. Companies could develop capabilities to support continuous engagement, such as through customer portals, to help agents identify these critical moments and start an insurance conversation at the right moment.

Personalise advice and planning

Infographics by McKinsey

Although financial planning is well established in many developed markets, the concept is relatively nascent in emerging Asia. But, as Asian consumers become wealthier and more sophisticated, they will look for agents who understand their needs, such as retirement planning and investing, and can provide bespoke advice. Insurers should tailor their financial-planning approach to the Asian context, where customers not only have less awareness of financial-planning options but also demand more flexibility in their financial-planning journeys.

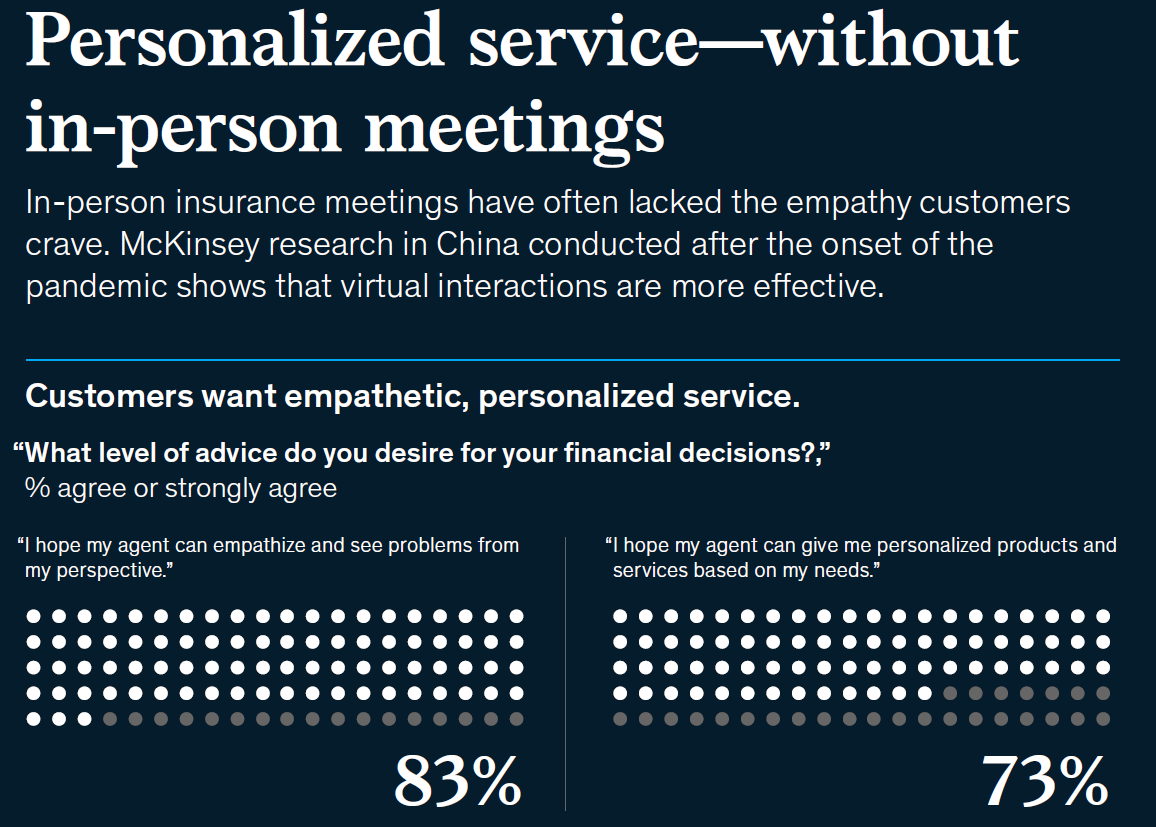

One approach might be to engage customers in discussions about their dreams and aspirations rather than asking for their data upfront. Interactive tools—that is, those built into existing sales tablets provided to agents—can help agents facilitate those discussions and map out aspirations and future priorities for their customers. Insurers can also explore additional digital tools to help agents better engage remotely with customers throughout their journeys. For example, some Asian insurers are launching remote advisory capabilities to enable agents to remotely underwrite policies and sign new customers. Artificial intelligence (AI)-enabled coaching, coupled with a remote advice platform, provides agents with personalised prompts based on real-time analyses of customers’ responses and agents’ performance metrics. Behavioural pairing models also use AI to improve the quality of customer–agent interactions by pairing them based on subtle behavioural characteristics.

Change agent value proposition

In many Asian countries, the capacity-led agency model encountered a bottleneck even before COVID-19. Leading insurers in large markets such as mainland China have reported stagnant growth in productivity and capacity due to new-agent attrition and a lack of professional field management, while smaller insurers look for ways to gain market share.

The new digitally enabled hybrid model will result in a gradual, enduring shift of the agent’s role from salesperson to financial adviser, in which he or she has expertise in products and financial planning. While this change will not happen overnight, it is imperative that insurance companies begin revisiting the compensation model to reward agents not only for acquiring new customers but also for providing quality advice to customers. Instead of paying agents solely on commission and overrides, insurers could incorporate fixed salaries and service- or activity-based bonuses into the digitally enabled hybrid model. By adjusting the incentives, insurers will encourage agents to get to know their customers and regularly stay in touch, creating deep and lasting customer relationships.

Provide modularised products with value-added services

Tech players are redefining what it means to integrate solutions more deeply within consumers’ lives to foster engagement. By rethinking product development, insurers could evolve from risk underwriters to partners that help customers become healthy and accumulate wealth. Insurers should develop customer-centric, proposition-led solutions that integrate insurance products with value-added services tailored to customers’ diverse needs. For example, one leading insurer recently launched an innovative critical-illness product for breast cancer with a wellness partner in Singapore, an integration of healthcare services such as preventive care, diagnosis, and recovery support.

Read also: Innovation at Ping An and the NextWave of insurance - EY Global Insurance Knowledge Leader

Improve flow of data and analytics

To enable omnichannel customer journeys, insurers and agents will need to enable cross-pollination of data at every touchpoint to ensure that customers can pick up right where they left off. Insurers should also identify analytics use cases along the customer journey and prioritise them based on their impact and ease of implementation. Examples of uses cases include using customer data from adjacent businesses or employing a customer-relationship-management tool to facilitate cross-selling and customise content for individual users across channels.

Adopt an agile way of working

Fostering rapid innovations and responding to new trends, regulations, and technology will also require an agile way of working. Insurers will need to shift from targeting large-scale developments while working in organisational silos to working in co-located, cross-functional teams using a flexible, test-and-learn approach. In agile ways of working, product development is done in short iterations with tangible results and a focus on continuous improvement.

Insurers should act now to plan for recovery from the pandemic and prepare for the shift to a new distribution operating model. Offering remote support to agents to improve customer engagement before and after sales and adopting digital tools to enable activity management and sales are critical to the successful adoption of the new model. Insurers that start early can emerge from the crisis better prepared to provide their customers with the products and services they need as the world moves into the next normal.

This article is brought to you by Bernhard Kotanko, Senior Partner, and Enoch Chan, Associate Partner, McKinsey

More from McKinsey:

What insurers can learn from China's continuing COVID-19 recovery - McKinsey

A New Industry Model for InsurTech - McKinsey

P.S: Join 10,000+ financial advisers, leaders, and senior executives on our complimentary VIP Weekly Newsletter

For the full suite of stories and updates, always check in to our Facebook / LinkedIn. Click the following if you want to improve your sales, learn how to be a better leader, or you just need some motivation to kick start your engine.

Do you have a new product or programme to share? Or perhaps you are keen to explore any collaborations with us or our partners? Reach out to us at Connect@AsiaAdvisersNetwork.com